Objective:

Learn various techniques to help meet minimum spend requirements often associated with new credit card sign-up bonuses, what to avoid when leveraging welcome bonuses, and the basics of manufactured spending.Learning Outcomes:

- Learn what a minimum spend requirement is, and how it relates to new card accounts and welcome bonuses

- Know some important considerations before applying for a new card product with a minimum spend threshold

- Learn some techniques to help meet spending requirements with little effort, and without overextending your spending power

- Learn the basics of online payment processors (third party payment options using credit cards)

- An introduction to manufactured spending

Suggested Prerequisites:

- Beginner’s Guide

- How To Access A Free Copy Of Your Credit Report

Introduction

Credit card bonuses are my favourite way to earn reward points easily and quickly. Welcome bonuses in Canada can range from 5,000-75,000 points, meaning one credit card application is often enough points for a round-trip flight, or more! Of course, nothing comes that easy, and many of the best offers have a minimum spend requirement in order to be eligible for the bonus points. In short, a minimum spending requirement is:A pre-determined amount of money that must be charged to the new credit card account within a set amount of time to be eligible for the sign-up bonus.

Rewards:

- 5x points on food & drinks

- 3x points on streaming services

- 2x points on gas, transit & ride sharing

- 1x points on everything else

- 15,000 points after your first purchase (no spend requirement)

- 15,000 points after your first purchase, with an additional 10,000 points after spending $1,000 in the first 3 months of account activation

- 25,000 points after spending $1,500 in the first 3 months of membership

- 60,000 points after spending $3,000 in the first 3 months of membership

- 75,000 points after spending $5,000 in the first 3 months of membership

5 Crucial Things To Remember When Trying To Meet a Minimum Spend Requirement

Before we look at ways to help meet spend requirements, there are some important considerations to remember:- Always remember to pay your credit card balances in full, each month, without fail. Taking advantage of credit card offers requires financial discipline, as carrying a balance and paying interest will take away all value in any reward. Never spend more than you can afford for a welcome bonus – it’s just not worth it!

- Don’t apply for more than you can handle. Credit card offers come and go, so don’t feel pressured to apply for more new products than you are comfortable spending on. Generally speaking, I only like to have one new credit card at a time, so I can focus all of my efforts towards hitting that minimum spend requirement

- The timeline for reaching a minimum spend starts at the time of approval, and not when you receive the card. While most cards will arrive within a week or two of approval, I’ve had some cards delayed over a month which really ate into my timeline. If in doubt, call your credit card provider and set a reminder for when the spending requirement is due

- If you don’t think you’ll make the deadline, don’t lose hope. Sometimes a simple call to the credit card provider will go a long way. I once forgot about a new card account I had, and a few weeks before the timeline was set to expire for the welcome bonus, I called in and the agent gladly extended the deadline as a courtesy because of my loyalty to the bank. While this may not always work, it’s worth a try as a last resort

- Don’t break the law. Ok, this may seem obvious, but a quick search on the internet will pull up a long list of the crazy stuff people have done to hit a spending requirement. Return fraud is a big one, where people will buy something fully refundable (an airline ticket, for example) and cancel or return the product/service after the bonus points have been posted. While definitely a grey area, morally and legally, I would strongly advise against it. Not only do you risk any consequences from the provider for returning something you never intended to keep, but you also risk losing the points if your credit card provider ‘claws’ them back with the return, or closes your account for violation of the terms and conditions.

3 Easy Ways To Hit a Minimum Spend and Get a Signup Bonus

The good news is most spend requirements are reasonable, with only a few offers in Canada requiring a lot of creativity if you don’t have a lot of purchasing power. For most Canadians, however, there are a few simple tricks that should ensure you reach the spending threshold for your welcome bonus!- Put all of your spending on the card you’re working towards passing a spend threshold. While this may seem obvious, it never surprises me when I hear ‘but this card gets me 2 points per dollar on gas’ or ‘this card has better purchase protection’ etc etc. While these are important considerations for everyday spend, forget all that when working towards a minimum spend requirement. Use that card for everything. Everything.

- Add a supplement card to your account. Better yet, add three or four or ten, especially if it’s a larger minimum spend. Of course, make sure it’s someone you trust entirely, like a spouse, family member, business partner, etc. Having two people will help hit the threshold twice as fast, three people three times as fast. Ten people? You do the math!

- Apply for new card products around big purchases. This is one many people overlook, and is maybe the most important. Some of the very best offers in Canada require hefty spend requirements to be eligible for the welcome bonus. Right now, I can think of more than one that needs $5,000 in the first 3 months. When I was new to travel hacking, this was daunting, especially since I had a modest income without a lot of disposable income. However, I still had some large annual bills that needed to be paid. Planning my applications around these large purchases enabled me to take advantage of offers I never would have been able to reach with my normal purchasing power. Some examples of large purchases you could plan your applications around include:

- Automobile insurance (pay in full, not monthly)

- Home insurance

- Property taxes (see next article)

- Personal income tax (see next article)

- Car Purchase

- Tuition (see next article)

- Home renovations

- Vacations

- Christmas

- Extended Health, such as braces

Most people have at least one or two of the above come up each year, so start planning your credit card application strategically to get the best bonuses!

Using Plastiq or PayTM Where Credit Cards Aren’t Accepted

You’re probably thinking:I’d love to pay income tax, property tax and tuition with my American Express, but none of those payees accept credit cardsYou’re right, kind of. While traditionally it’s been impossible to pay taxes, utilities and tuition with credit cards, there are new online services that allow you to pay basically any service provider with Visa, Mastercard and American Express. Two examples of these online payment processors in Canada are: In essence, these third party payment processors accept your credit card for payment and send a cheque or money transfer to the service provider you want to pay. Simple as that! Of course, someone has to pay for this convenience, and it’s always the service user. Fees vary depending on who you’re paying, what kind of card, and any promotions being offered. At the time of publishing this lesson, Paytm is offering 0% transfer fees on all transfers up to $1,500 per day, which is incredible! Generally though fees range from 0-2.5 percent, which can quickly eat into any value in the rewards earned. Let’s look at an example of how this could work, even if you did need to pay fees. Tyler just got his Notice of Assessment from the Canada Revenue Agency. Turns out Tyler owes $5,000 this year, and needs to pay by the end of April to avoid paying fees. Tyler decides to look at current credit card offers and sees that American Express is offering 30,000 Membership Reward points as a welcome bonus after spending $5,000 in the first 3 months of membership on The Business Gold Rewards Card. Tyler decides to apply for the card knowing he has the cash in the bank to pay the bill and would rather get some points out of it! Tyler uses Plastiq, because they are one of the merchants eligible for 2 points for every dollar spent on the Business Gold Rewards Card. To add Plastiq as an eligible merchant, Tyler needs to go through the American Express online services. Once that’s done, Tyler quickly makes a Plastiq account, and enters all of his payee information (The CRA in this case).

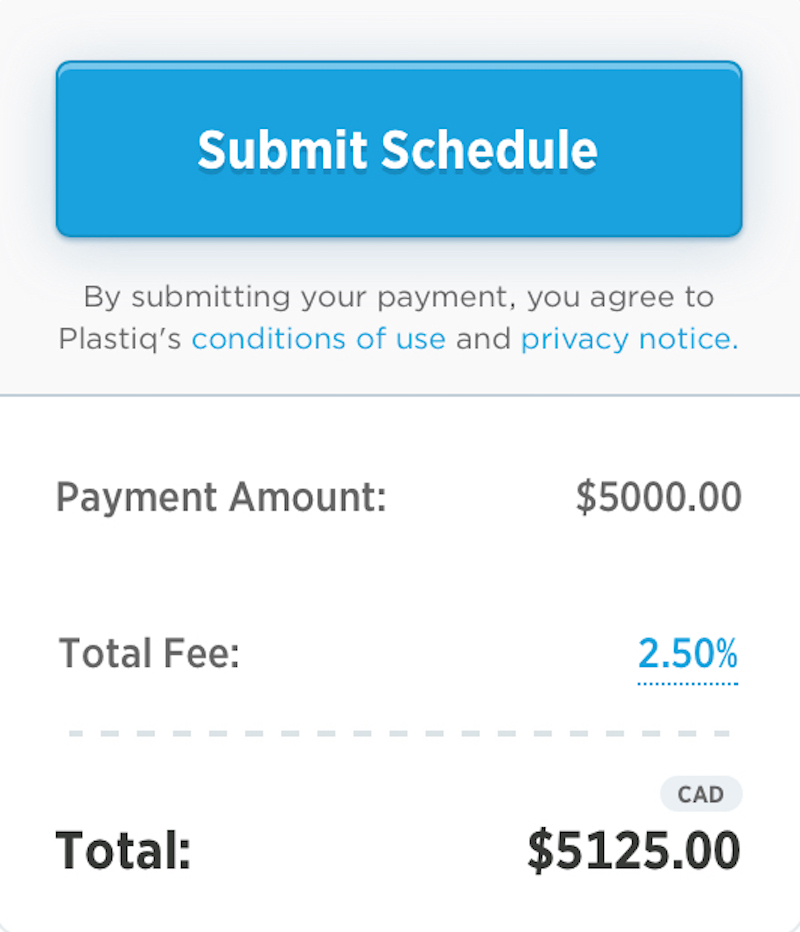

Then he enters a bit of personal info, his credit card information, and comes to the final screen. There is a %2.5 fee for payments to the CRA through Plastiq using an American Express card, but Tyler considers that fair value in this case since he will get 2 points for every dollar (10,000 points) and meet the minimum spend requirement with one transaction.

Then he enters a bit of personal info, his credit card information, and comes to the final screen. There is a %2.5 fee for payments to the CRA through Plastiq using an American Express card, but Tyler considers that fair value in this case since he will get 2 points for every dollar (10,000 points) and meet the minimum spend requirement with one transaction.

While the fee is $125 dollars, Tyler values Membership Reward points at more than 2 cents per point when transferred to a frequent flyer participant, so he considers this very good value. Even if redeemed for a statement credit towards a purchase, the points earned for this single transaction (10,000) would be nearly enough to cover the entire fee, making for a near breakeven transaction. Tyler was also able to meet the hefty minimum spend requirement with a single transaction!

While the fee is $125 dollars, Tyler values Membership Reward points at more than 2 cents per point when transferred to a frequent flyer participant, so he considers this very good value. Even if redeemed for a statement credit towards a purchase, the points earned for this single transaction (10,000) would be nearly enough to cover the entire fee, making for a near breakeven transaction. Tyler was also able to meet the hefty minimum spend requirement with a single transaction!

What Is Manufactured Spending and Should You Do It?

Manufactured spending, or MS for short, is a bit of a controversial subject. While not illegal, it definitely straddles the boundaries of most reward programs terms and conditions and is not a strategy I employ in my efforts to earn points, though I have practiced ‘kind of variations’ (more on that below) of MS when I was new to travel hacking. In short, Manufactured Spending is:The process of putting through a large volume of spend on your credit card without actually spending any money. The simplest way is to buy items that can be easily converted into cash to pay off your credit card balance in full before the statement closes.Confused? You should be, as manufactured spending generally involves loopholes and processes that wouldn’t normally come to mind for the everyday consumer. I’ll use a real-world example that was available to Canadians up until recently:

The Canadian Mint used to sell face value coins to the public and provided free shipping anywhere in Canada. The coins were limited edition and only a set amount per household could be ordered per release. That being said, the Canadian mint usually had anywhere between $2,000 and $3,000 in face-value coins available for purchase in various denominations, ranging from 20-100 dollars. Because they are technically legal tender, banks had to accept them at their face value. So, anyone could order $2,000-$3,000 worth of coins, tax-free, without shipping costs on their American Express or any other credit card and bring the coins to the bank upon delivery and exchange them for cash. In this example, you are basically buying cash with your credit card, earning reward points, without any cost to you (except for the time spent).This went on for years with The Mint, with a lot of travel hackers cashing in thousands of dollars in coins per month. The Canadian mint recently discontinued the face-value coin program (gee, I wonder why), and the opportunity ended for Canadians to earn thousands of points per month for buying cash on their credit cards. How have I used manufactured spending in the past? I’ll give you two examples (I had a lot more free time when I did this):

Back when Costco accepted American Express cards for online purchases, I would buy Costco gift cards at face value and sell them on eBay. For whatever reason (I’m still not entirely sure why), Costco cards (and other gift cards) sell above face value on eBay, which pays for all of the shipping and transaction costs as a seller. So, I could buy a $500 Costco gift card with my credit card, sell it on eBay for $600, and then pay off my credit card and pocket $20-$50 after all the transaction fees were accounted for. While this was certainly an easy way to make a few thousand points per month (and a few hundred dollars), it ended up being too time consuming (you wouldn’t believe how many questions I would get asking where I got off selling gift cards above face value).Also…

A few years ago I came across a promotion to buy the iconic HBC Point Blanket at a substantial discount. These blankets rarely go on sale, meaning they can usually be sold at retail price on eBay. I was able to stack the annual sale with another coupon, and this netted a 35 percent discount off the retail price. I would then turn around and sell the blanket on eBay at full price, and again make $50-$100 per transaction per blanket plus the points earned for purchasing the blankets with my Amex (they aren’t cheap – this was a great way to earn points). What made this even more lucrative is that HBC is an online retailer with the Aeroplan eStore. HBC would regularly run promotions for 5X the Aeroplan points for every dollar spent, and I was easily earning 20,000-30,000 Aeroplan miles per month reselling blankets! Like the Costco gift card game, this was time consuming, and I actually started to run into inventory problems with HBC. There were also a couple of times the blankets didn’t sell fast and I was stuck paying the credit card balance before they sold.There are countless other methods one could employ if they really wanted to get into MS, and I’ll explore some of those options in an upcoming advanced level course. Manufactured spend techniques are usually short-lived however, as banks and retailers often close loopholes once discovered. I generally find most MS opportunities too time consuming now, but there are some great opportunities for those with more time than purchasing power, or those who like to flex their creativity in an effort to outsmart the system!